Federal Budget Update – Make It Make Sense

The 2026 Federal Budget has certainly given accountants plenty to talk about.

From changes to personal tax, discretionary trusts, capital gains tax, negative gearing and small business concessions, 2026–27 Federal Budget introduces some significant reforms that could affect individuals, investors and business owners over the coming years.

If you've seen headlines about the "death of discretionary trusts" or "the end of negative gearing", don't panic just yet. Many of these measures won't commence for another year or two, and several are still subject to consultation and legislation.

Let's break down the key changes and what they could mean for you.

What's the Big Theme of the 2026 Budget?

The Government has positioned this Budget around the concept of intergenerational fairness and creating a tax system that treats income from investments and business structures more similarly to employment income.

In simple terms, many of the measures aim to reduce situations where people using trusts or investment structures pay less tax than someone earning the same amount through wages and salary.

Whether you agree with the approach or not, it helps explain why so many of the proposed changes focus on trusts, capital gains tax and property investment.

Good News for Employees

Not every Budget announcement is scary.

There are a few measures designed to put more money back into the pockets of workers.

1. A New $250 Working Australians Tax Offset

From 1 July 2027, most taxpayers earning employment income, sole trader income or personal services income will be eligible for a $250 tax offset. The Government estimates this will apply to around 97% of taxpayers.

Example:

Pete works as an artist and earns $85,000 per year.

Under the proposed changes, Pete may receive a $250 tax offset when lodging his tax return, reducing the amount of tax payable. Offsets are more beneficial than deductions because they reduce the tax bill $ for $. That is $250 off what would have been the tax bill.

It's not life-changing money, but we'll take every dollar we can get.

2. A Flat $1,000 Work-Related Deduction

From the 2026–27 income year, the Government is introducing a $1,000 Instant Tax Deduction for work-related expenses. Taxpayers can choose a standard $1,000 deduction for work-related expenses without needing receipts or substantiation.

Example:

Charlotte usually claims:

Uniform expenses

Professional memberships

Phone costs

which total around $700 each year.

Instead of collecting receipts and records, Charlotte may simply choose the $1,000 standard deduction.

However, if your expenses are over $1,000 - say, you bought a camera, new software, or studio gear - you can still claim the amount the usual way.

You can also still claim charitable donations, union fees, and professional memberships on top of this $1,000 deduction. It doesn’t eat into those.

3. Small Income Tax Cuts

The tax rate applying to income between $18,200 and $45,000 will gradually reduce over coming years.

While modest, these changes provide ongoing tax relief for lower and middle-income earners.

Small Business Wins

Now for some good news for business owners.

-

Permanent $20,000 Instant Asset Write-Off

One of the most welcomed announcements is making the $20,000 instant asset write-off permanent for eligible small businesses.

Eligible businesses with turnover under $10 million can immediately deduct assets costing less than $20,000 on a per-asset basis.

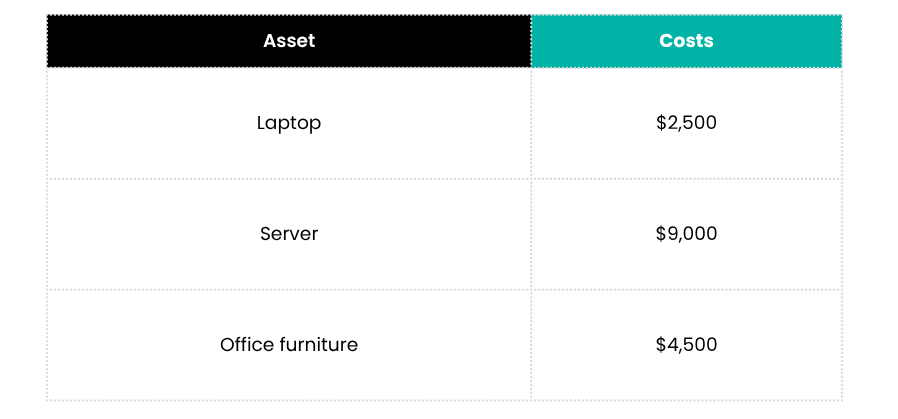

Example:

Dell owns a small IT business. During the year, he purchases:

Because each asset costs less than $20,000, Dell can potentially claim an immediate deduction rather than depreciating them over several years.

For cash flow, that's a huge win.

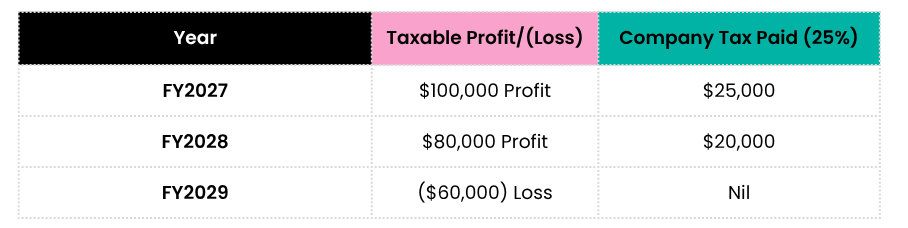

- Two-Year Loss Carry-Back

The Government is also making loss carry-back measures permanent for eligible companies.

This allows companies to offset current losses against tax paid in previous years and potentially receive a refund.

Example:

Naomi owns a physiotherapy clinic that operates through a company.

- The loss would generally sit there until future profits are earned.

- Naomi receives no immediate benefit.

With loss carry-back:

- The loss may generate a tax refund now.

- The company gets cash back when it likely needs it most.

Think of it as the ATO giving back some of the tax you paid during the good years to help you get through the tougher ones.

- Electric Vehicle Benefits Are Staying... For Now

The current Fringe Benefits Tax (FBT) exemption for eligible electric vehicles is not disappearing immediately. Instead, it will be phased down over time.

Example:Charlotte decides to salary package an electric vehicle.If she enters into the arrangement before the end of the current concession period, she may continue receiving more generous FBT treatment than someone entering into a similar arrangement several years later.

The Big One: Discretionary Trust Changes

This is the measure that generated most of the headlines.

From 1 July 2028, the Government proposes introducing a 30% minimum tax on discretionary trusts. The trustee would pay the tax, while beneficiaries receive non-refundable credits for tax already paid by the trust.

Why Is This Happening?

The Government argues that discretionary trusts allow income splitting among family members, which can result in lower overall tax compared to wage earners with similar income levels.

Example:

Cooper operates his business through a discretionary trust.

Historically, the trust distributes income between:

- Cooper

- Charlotte

- Violet

based on who has the lowest tax rates each year.

The proposed minimum tax is intended to reduce the tax advantage of those arrangements.

Is This the End of Trusts?

Not necessarily.

Trusts still provide:

- Asset protection

- Succession planning benefits

- Estate planning flexibility

However, some structures may become less tax-effective than they are today.

The Government is also proposing a three-year restructuring relief period beginning 1 July 2027 for businesses that wish to move into other structures such as companies or fixed trusts.

Capital Gains Tax Changes

Another major reform is the proposed replacement of the current 50% CGT discount.

From 1 July 2027:

- Existing gains accumulated before that date retain current treatment.

- Future gains will move to an indexation-style system.

- A minimum 30% tax rate may apply to real gains.

Importantly, past gains are protected under the transitional arrangements.

Example:

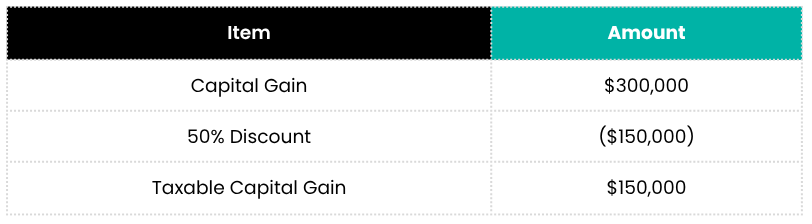

Addison purchased an investment property in July 2020 for $500,000.

By July 2030, she sold it for $800,000, resulting in a gain of $300,000.

Under the current rules

Because Addison owned the property for more than 12 months, she may be eligible for the 50% CGT discount.

Addison only includes $150,000 in her tax return.

Under the proposed rules

Instead of automatically receiving a 50% discount, the cost base may be adjusted for inflation first, with the new CGT rules applying to future gains from 1 July 2027.

The exact tax outcome will depend on inflation and future legislation, but the key takeaway is:

The current automatic 50% discount may no longer apply to gains accumulated after 1 July 2027.

Simpler explanation

Before:

"You made a gain? Here's a 50% discount."

After:

"Let's first work out how much of that gain is genuine growth versus inflation."

Small Business CGT Concessions Remain

One of the most important points that many headlines missed:

The four Small Business CGT Concessions remain available.

This means many eligible business owners may still:

- Reduce capital gains

- Defer gains

- Potentially eliminate gains entirely

when selling an active business.

For many small business owners, this is arguably more important than the broader CGT reforms.

Example:

Sam owns a physiotherapy clinic. He started the business years ago and plans to retire.

The business is worth $1.5 million and has grown significantly since he started it.

When Sam sells the business, he may still be eligible for the existing Small Business CGT Concessions if he meets the requirements.

These concessions can potentially:

- Reduce the capital gain

- Defer the gain

- In some cases eliminate the gain completely

Why this matters

Many small business owners hear:

"The CGT discount is changing."

And immediately think:

"Oh no, I'm going to pay hundreds of thousands more tax when I retire."

Not necessarily.

For many eligible small business owners, the Small Business CGT Concessions are actually much more valuable than the standard 50% discount.

Negative Gearing Changes

The Budget also proposes significant changes to negative gearing.

For residential properties acquired after 12 May 2026, negative gearing concessions may be restricted unless specific conditions are met, with losses instead carried forward for future use.

Example:

Sheldon buys an investment property after 12 May 2026.

For the year:

Under current rules

Sheldon may generally use that $10,000 rental loss to reduce his salary income.

If Sheldon earns:

This means he pays less tax immediately.

Under the proposed rules

The $10,000 loss may no longer be able to immediately reduce his salary income for certain newly acquired residential properties.

Instead, the loss may need to be carried forward and used in future years.

Sheldon pays more tax now, but the loss isn't lost. It simply sits there and may be used later when the property becomes profitable or is sold.

Simple explanation

Before: Lose money on your rental property and receive a tax benefit now.

After: Lose money on your rental property and receive the tax benefit later.

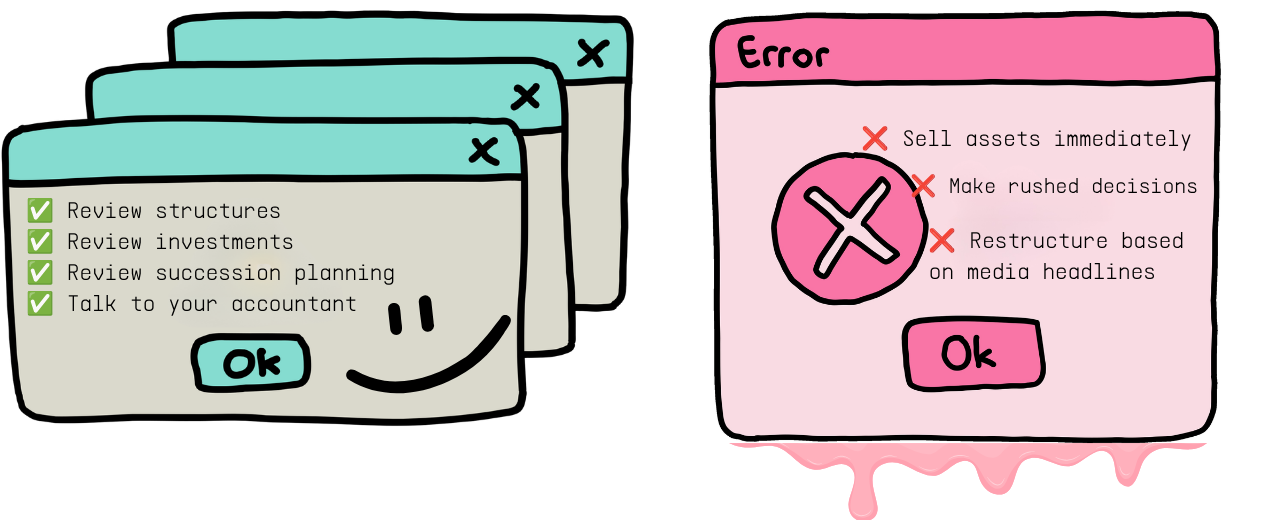

What Should You Do Right Now?

For most people, the answer is simple:

Don't panic. Don't restructure tomorrow. Don't sell assets tomorrow.

Many of these measures:

- Start in 2027 or 2028

- Require legislation

- Are still subject to consultation

- May change before implementation

Instead, now is the time to:

- Review your business structure

- Understand how trusts are currently being used

- Consider future succession plans

- Review investment strategies

- Speak with your accountant before making major decisions

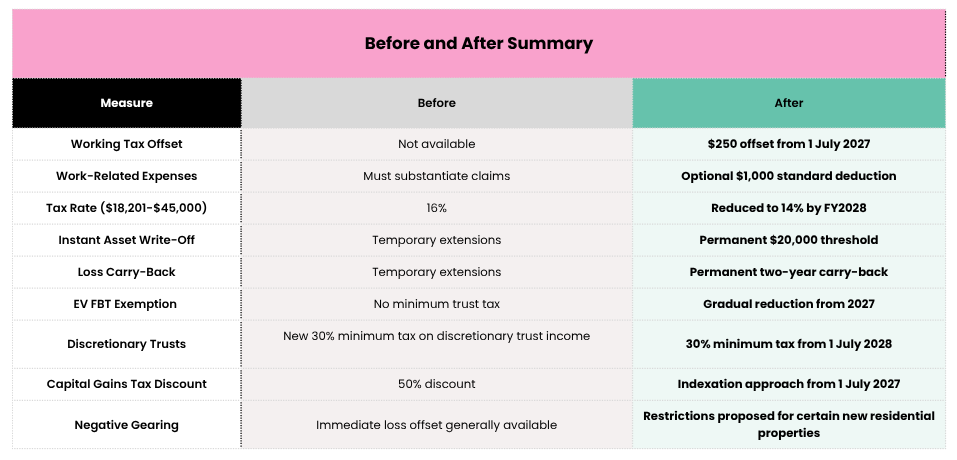

Before vs After Summary

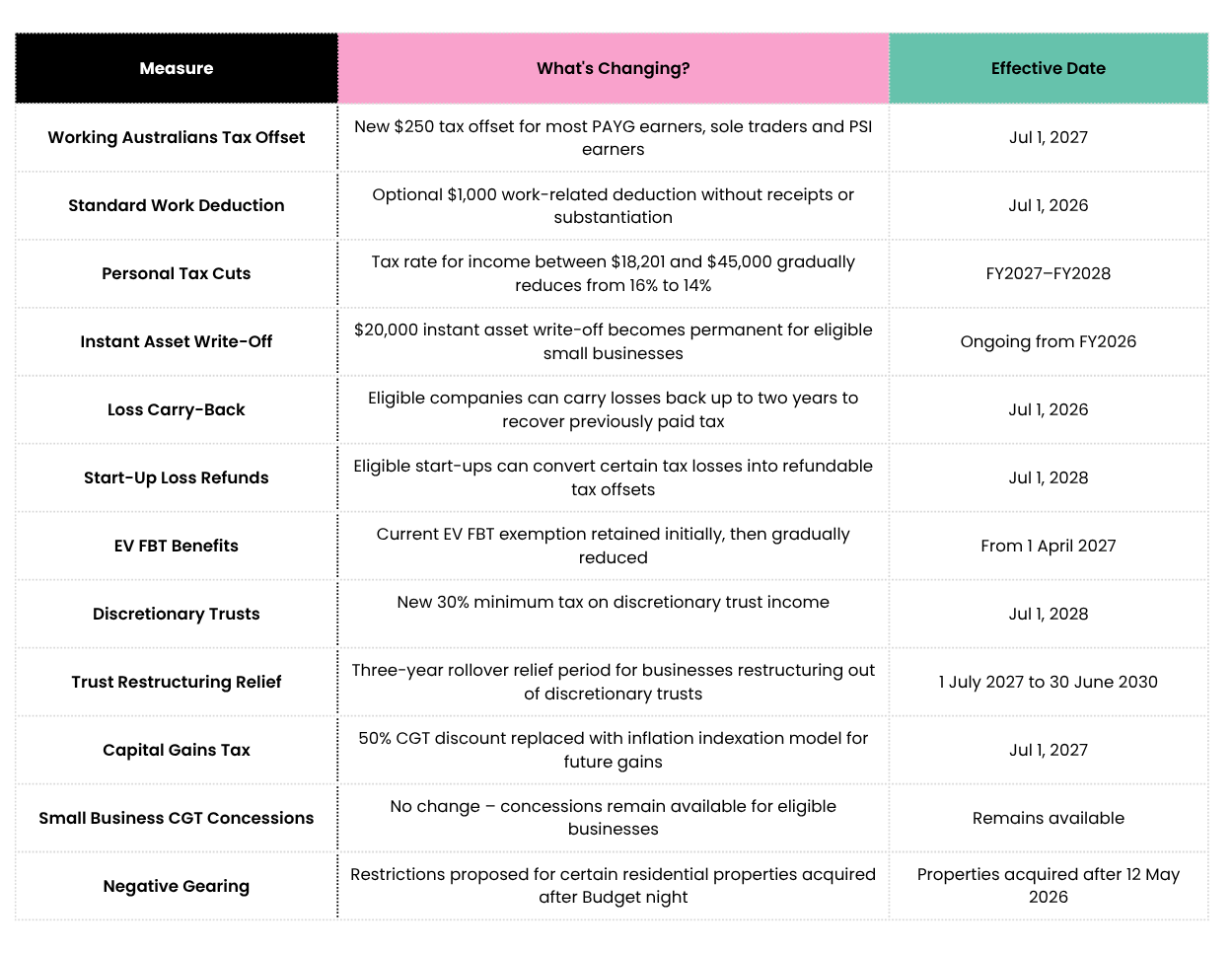

TL;DR – 2026 Federal Budget Cheat Sheet

The Bottom Line

The 2026 Federal Budget is one of the most significant tax reform packages Australia has seen in recent years.

While some measures provide welcome relief for workers and small businesses, others could fundamentally change how trusts, investments and capital gains are taxed.

The key takeaway? Most changes are not happening tomorrow.

There is still time to understand the reforms, seek advice and plan appropriately.

As always, good tax planning is not about reacting to headlines. It's about understanding the rules, considering your circumstances and making informed decisions before changes take effect.

References

2026 Federal Budget - Webinar | Accountants Daily

Tax reform | Budgets.Gov

2026 Federal Budget overview – After the dust has settled- Webinar | CCH Learning